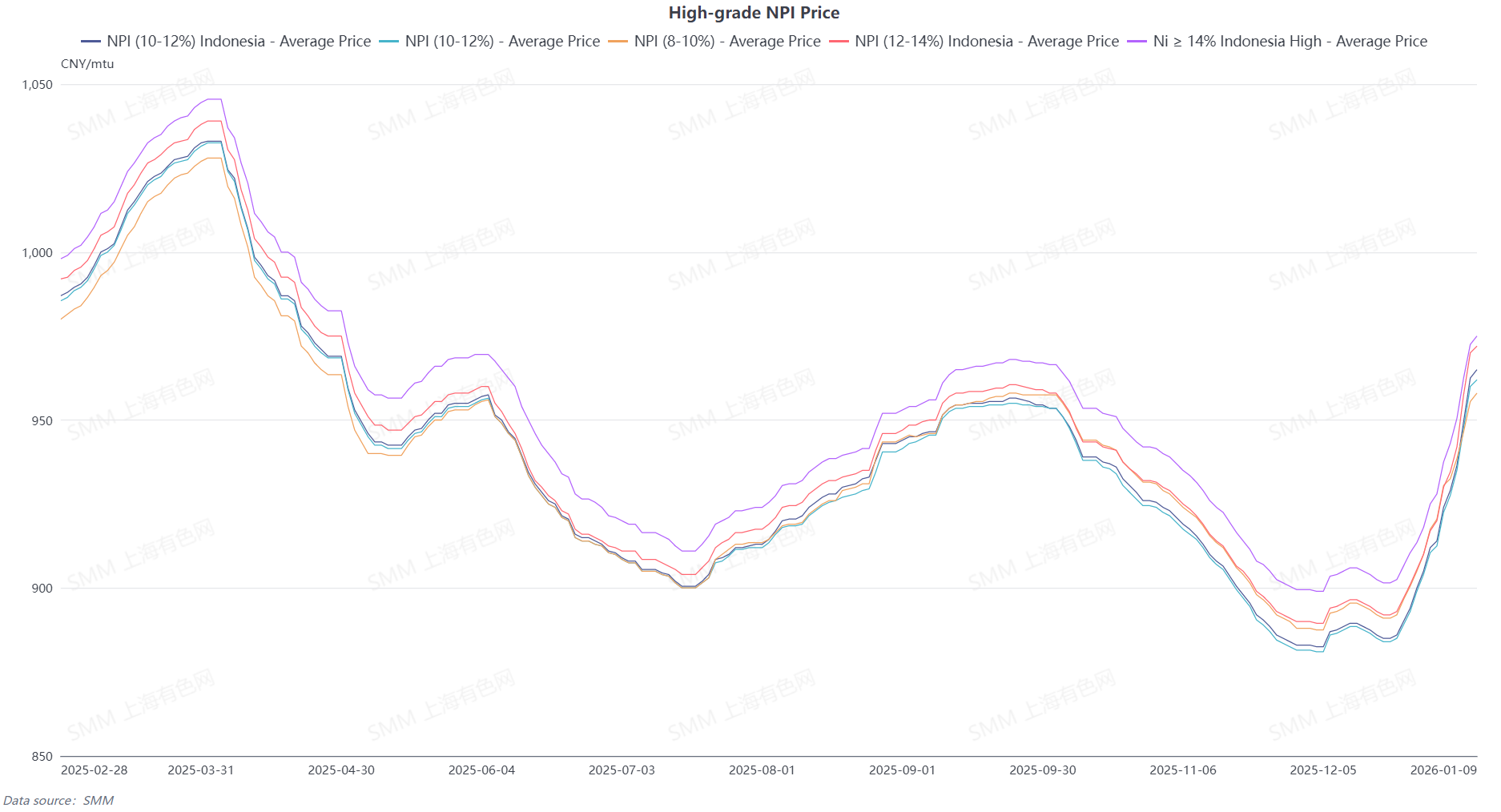

The average price of SMM 10-12% high-grade NPI rose 31.23 yuan/mtu WoW to 946.4 yuan/mtu (ex-factory, tax included), while the average Indonesia NPI FOB index price increased 4.26 $/mtu WoW to 118.92 $/mtu. This week, futures retreated after a rapid rise, and the price spread between futures and spot high-grade NPI widened significantly during the week, reaching a relatively high level, triggering market arbitrage positioning.

Supply side, upstream sentiment is strongly bullish, smelters actively hold prices firm, and market offers continue to climb. Additionally, production halts at some Indonesian iron plants may be difficult to resume in the short term, leading to a certain decline in market supply. Demand side, downstream sectors remain in the traditional off-season, and end-use demand is limited. However, driven by the rise in futures, stainless steel enterprise profit margins improved, and intended prices also moved higher. Overall, amid the weak supply-demand pattern, due to arbitrage activities by some traders, a large amount of high-grade NPI supply is difficult to release, resulting in tight spot supply in the market in the short term. Looking ahead, high-grade NPI prices are expected to remain supported by macro and fundamental factors in the short term, and prices are projected to have further upside room.

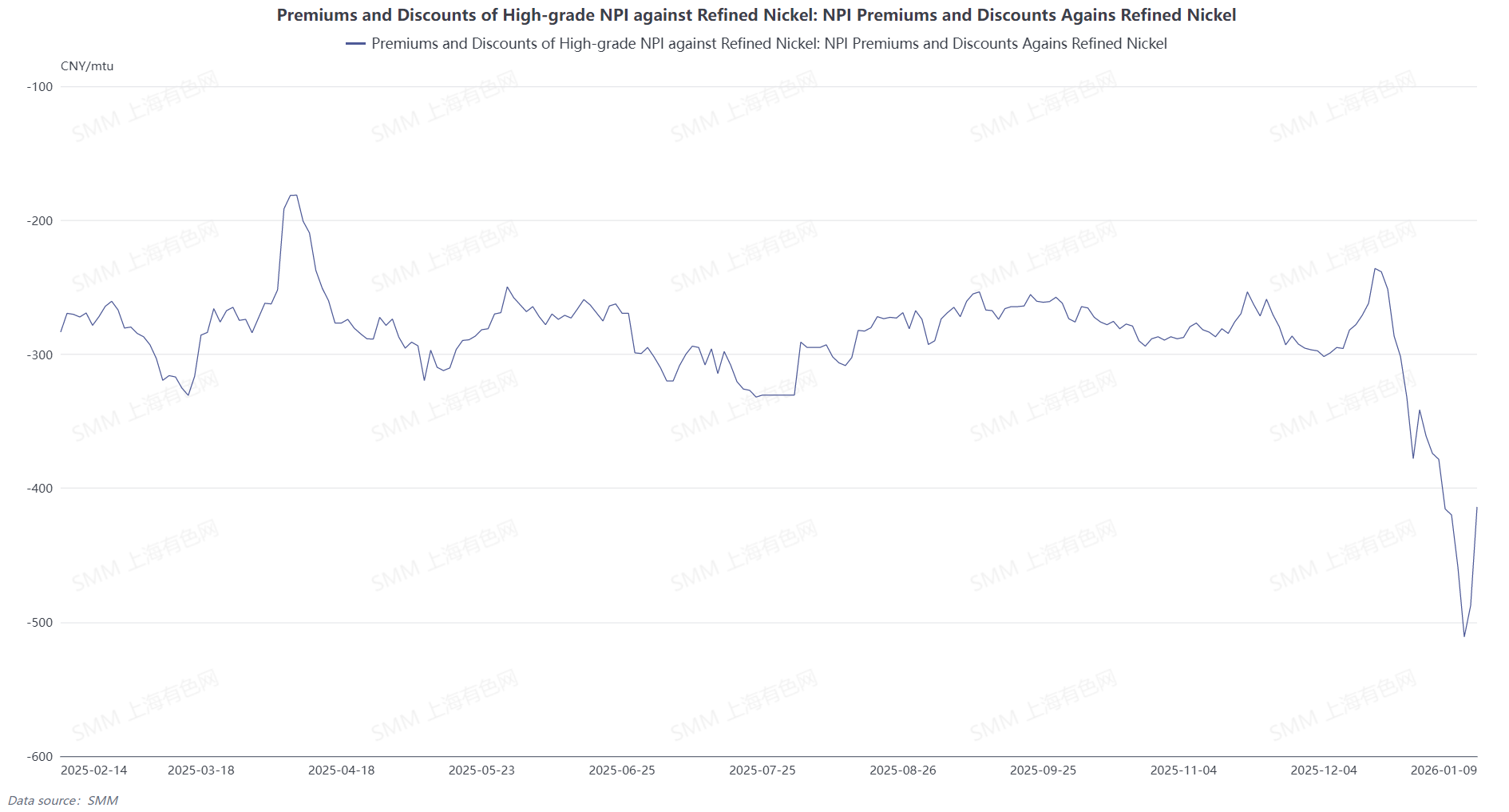

From the perspective of NPI conversion to high-grade nickel matte, refined nickel prices continued to rise this week, and high-grade NPI prices also increased WoW. The average discount of high-grade NPI to refined nickel widened to 458.3 yuan/mtu. High-grade NPI is expected to maintain its upward trend next week, while the average refined nickel price is expected to pull back slightly. The average discount of high-grade NPI to refined nickel is projected to gradually narrow, but profitability for converting NPI to high-grade nickel matte remains high.

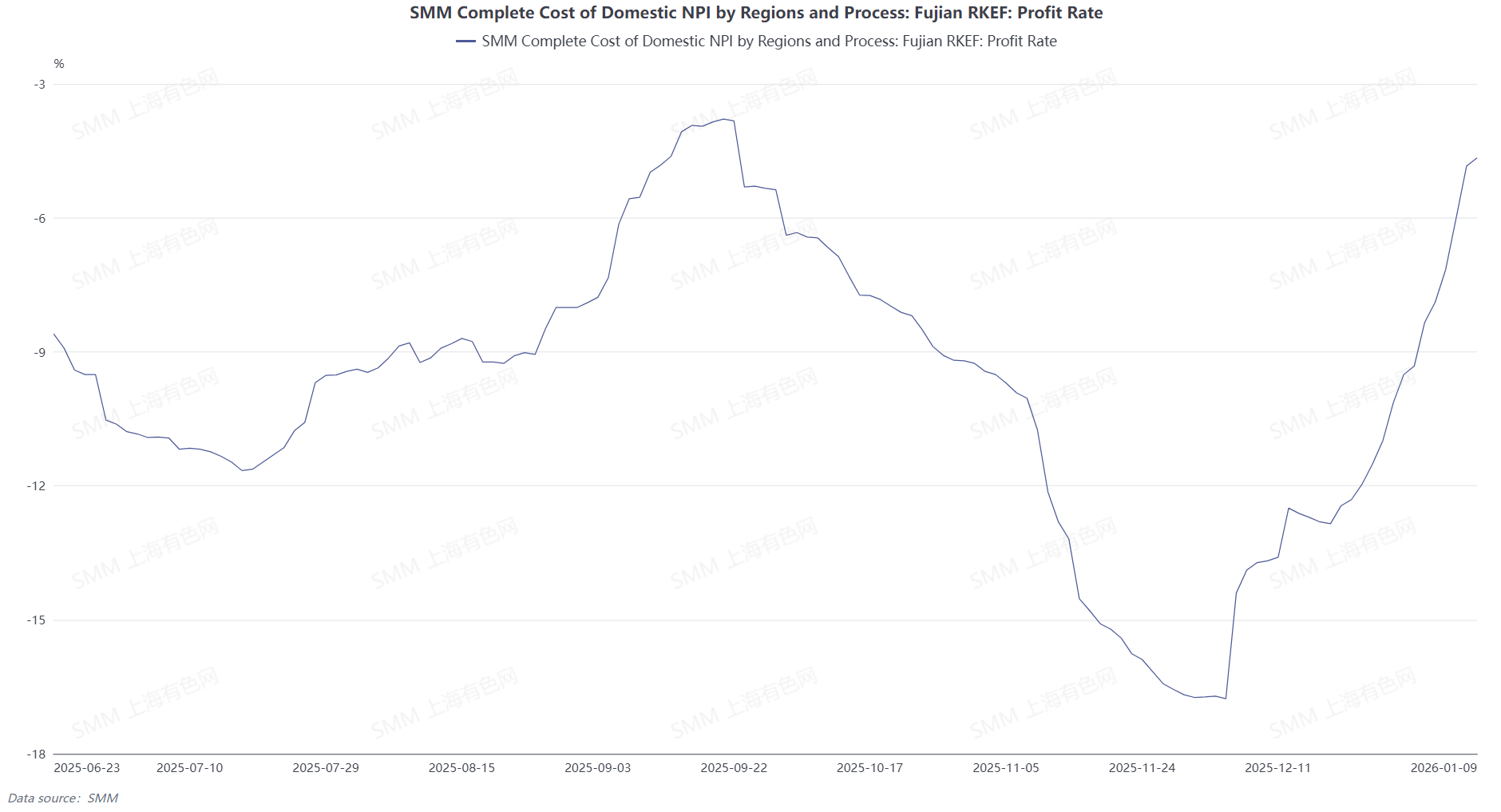

Based on the nickel ore prices from 25 days ago, the cash cost for high-grade NPI was calculated. This week, smelter margins for high-grade NPI continued to recover. Raw material side, ore prices from Indonesia and the Philippines held steady, while auxiliary material prices declined, leading to a continued slight decrease in the production cost of high-grade NPI. Concurrently, high-grade NPI prices continued to rise, improving smelter margins. Looking ahead to next week, raw material side, ore prices are expected to remain stable, auxiliary material prices are expected to be relatively flat, and high-grade NPI still has upside room. Smelter margins are expected to continue increasing.